Credit Suisse has released a report entitled "Is the commodity supercycle behind us?" by Dong Tao. This report has a couple of important points, but misses several key items. But what does the report say?

The following is from the summary:

"We believe the golden age of infrastructure investment is behind

us now. The golden age of housing boom is behind us now. The

golden age of export is behind us now. The golden age of policy

stimulus is behind us now.

● But, one more leg of urbanisation is expected. Further

acceleration in policy housing is likely.

● Still, trend growth in the next decade is projected at 7–8% versus

10.3% in the past decade. Growth engines will shift from exports

and infrastructure to consumption, which means that it will take

less commodity consumption for each unit of GDP."

First, we need to see that commodities are not all identical. One key difference between commodities is 'capital commodities' vs 'consumption commodities'. Capital commodities are not used up and continue to exist for many years. For example, copper wire is produced and used for many years. It then can be melted down and re-used. It is a 'Capital commodity'. Other commodities like this are Gold, silver, aluminum, iron and to some extent steel. The use of the commodity continues for many years. In contrast 'consumption commodities' are consumed. Oil is consumed and cannot be 'resused' or used more than once. You go to the store in a car and gasoline is consumed and can not be 'resused' or used for many years. Likewise the soft commodities like soybeans are consumed.

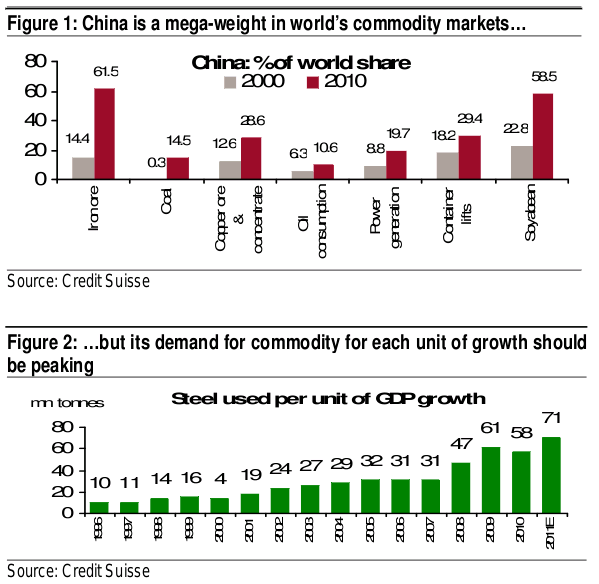

In this article, the author makes no distinction between capital commodities and consumption commodities. Look at the following chart and notice the products along the bottom:

Do you see that copper is not the same as soybeans? If the statement about the 'age of infrastructure are true, copper demand might change. But why would soybean demand decrease because infrastructure investment decreases? The argument just does not hold. In fact, I would argue just the opposite. As the age of infrastructure is over, the age of consumption starts. In the age of consumption, consumption commodities will be in MORE demand than in the age of infrastructure. Soybeans and oil are will be in MORE demand than before.

Second, the law of growth is important. Let's use a simple example. If you start out at 100 on an measure of economic activity and that economic activity requires 10 units of 'commodities'. If you grow by 10%, that would increase your commodity demand by 1 (assuming the same ratio). Now assume the economy grows by 10% for 10 years. At the end of ten years, the index is at 235. Now assume the growth rate falls to 7%. The INCREASE in commodity demand, assuming a constant ratio is still 1.65 and is MORE than the INCREASE in demand for most years. The TOTAL demand for commodities is now 25.2, up from 10 in the first year. Do you see that the growth of the economy means that ZERO growth, does not decrease the 25.2 demand for commodities, but only decreases the 'growth rate of demand'. That is totally different than decreasing demand.

Thus, we have the Chinese economy about the change gears (if the CS author is correct about that), but that has vastly different implications for different commodities. As people achieve basic stability and economic prosperity, they start to have different demands. For example, the demand for jewelry and other high fashion will increase. Likewise the demand for more complex meals will increase. This will change the type of commodities that are demanded. Steel demand will decrease. But gasoline demand may skyrocket as people begin to buy cars and take vacations. Why work 80 hour weeks if you can't ever take a vacation? The demand for airtravel will increase and the demand for jet fuel will increase.

Thus a changing Chinese economy will have massive impacts on the price of commodities, but it will not all be bad. Some commodities will see skyrocketing demand, while others may see demand stay level.